Divorce can be one of the most emotionally challenging experiences a person goes through, with the heartache often extending into unexpected corners of life—like finances. One aspect often overlooked is the hit your credit score might take as a result. While the act of getting divorced doesn’t directly affect your credit score, the financial ripple effects can be devastating. The emotional toll of a breakup is hard enough, but when your financial world begins to unravel as well, it can feel like a double blow.

Many people enter marriage with the expectation of sharing everything, including finances. When that bond breaks, separating your financial life can be as difficult as untangling your heart. Credit cards, mortgages, auto loans—these joint accounts, which may have once symbolized a shared future, become a battleground for responsibility. Even after the ink on your divorce papers dries, your financial obligations from your marriage remain. If your ex misses a payment on a joint account, your credit score can take a hit, regardless of your awareness or involvement. It’s a painful reality, one that feels unfair, adding stress to an already overwhelming situation.

Financial strain after divorce is common. The sudden shift from a dual-income household to managing expenses on your own can leave you feeling financially stranded. Legal fees, child support, alimony—these new burdens can make it difficult to stay on top of regular bills like rent, utilities, or credit card payments. And when you’re trying to emotionally heal, financial slip-ups can feel inevitable. But even a single missed payment can send your credit score plummeting, making it harder to rebuild your financial life.

The emotional whirlwind of divorce can also lead to an increase in debt, particularly if you’re using credit cards to cope with unexpected costs or relying on loans to make ends meet. This mounting debt not only adds to your financial burden but also raises your debt-to-income ratio. The higher that ratio climbs, the more it feels like a noose around your neck, tightening as your credit score takes a dive. As if the pain of losing a relationship wasn’t enough, now you’re losing access to the financial stability you once had.

For some, divorce leads to financial situations so dire that bankruptcy seems like the only way out. Declaring bankruptcy is a final, heartbreaking blow to your financial reputation. It’s a decision often made out of desperation, but one that lingers, staining your credit report for up to a decade. A hit like this can feel like starting over from square one, just as you’re trying to put the pieces of your life back together.

However, there is hope. Just like with emotional healing, financial recovery takes time and care. While divorce can make your financial world feel like it’s crumbling, taking deliberate steps can prevent it from falling apart entirely. Closing joint accounts, refinancing shared debt, and keeping a close eye on your budget are crucial. You can’t control what happens with your ex’s finances, but you can control your own. By creating a solid financial plan and seeking support, you can start rebuilding not only your life but also your credit score.

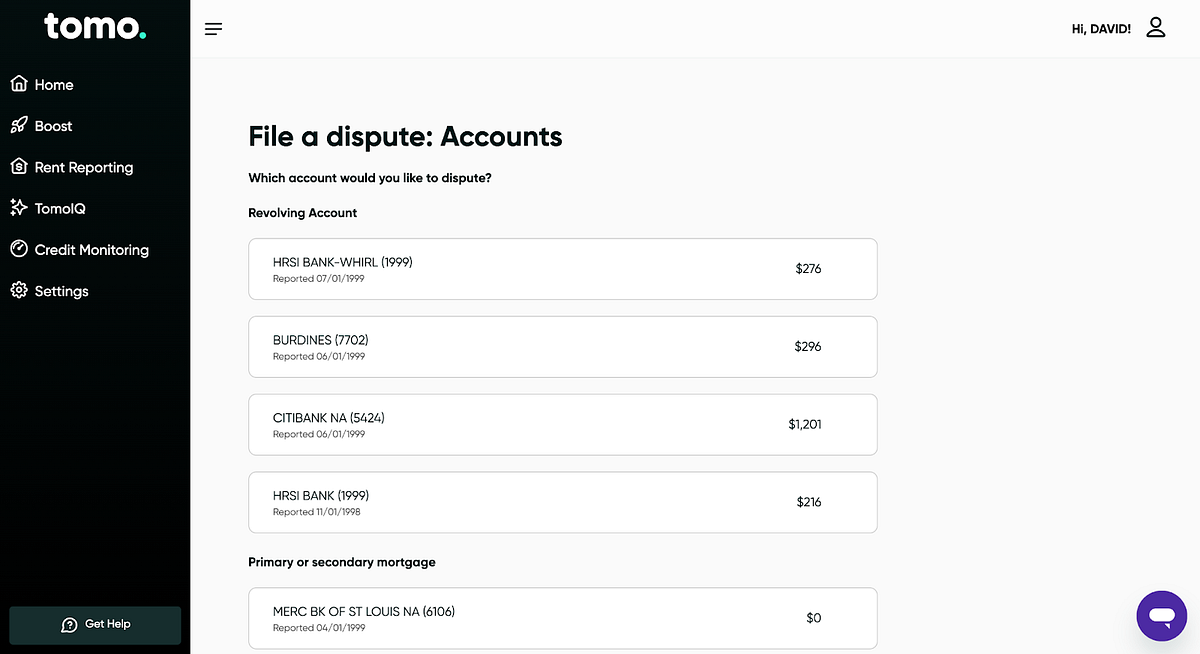

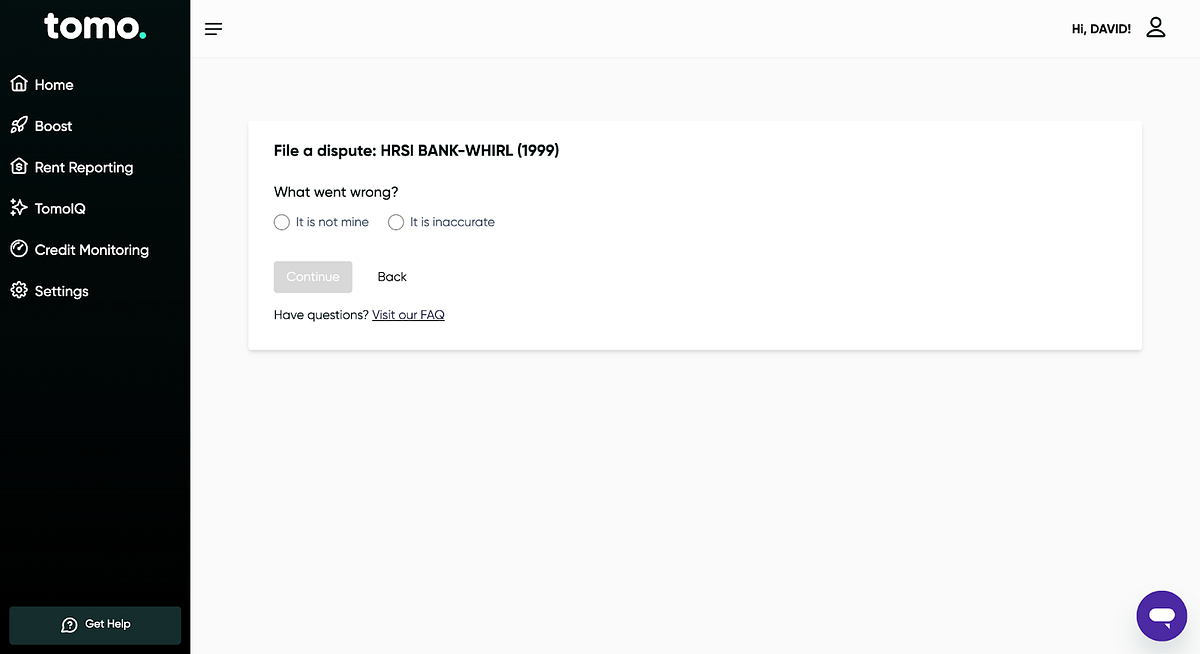

At TomoCredit, we understand that recovering from divorce is not just about healing emotionally but also about repairing your financial foundation. That’s why we offer a Credit Error Dispute Service—an essential tool to help you correct inaccuracies on your credit report that shouldn’t be there. Divorce is messy, and credit mistakes are common, especially when accounts and responsibilities get tangled. Our service works to dispute these errors, ensuring your credit report accurately reflects your financial reality, not the residual effects of a relationship that has ended. By resolving these disputes, you can speed up your credit recovery, helping you regain control over your financial life when you need it most.

Rebuilding after a divorce is a journey of resilience. It’s about picking yourself up, bit by bit. Credit scores, like emotional scars, take time to heal, but with careful attention and patience, you can recover. Paying off debts, avoiding late payments, and exploring options like secured credit cards can help you slowly but steadily regain financial stability. With TomoCredit’s support, you can make sure that errors don’t stand in the way of your progress.

In the end, divorce doesn’t just break hearts—it can break credit too. But just as you will heal emotionally, your credit score can also bounce back with time and diligence. The road to recovery may be long, but it’s not one you have to walk alone. Let TomoCredit help you take control of your financial future, providing the tools you need to protect your credit and rebuild after this significant life event.