Whether you are a student getting ready for college, a current college student, or a parent of one, you may be eligible for a federal student loan. Although your financial aid office will issue you student loans according to the documents you submit, you have the option to reject or consult with your advisor for another type. You may ask — why would I reject any student loans? Isn’t more the better? Different types of student loans come with different obligations on the repayment process that you may rather not accept.

Here are the two types of basic student loans:

Direct Subsidized Loan

The direct subsidized loan is given based on financial need — which the Department of Education defines as “The difference between the cost of attendance at your school and you expected family contribution.” In other words, the documents you issue to your school, like your family’s tax filings, are essential.

A key factor to this type of loan is that the federal government will pay for the interest accrued while the student is in college, and for the first six months after you leave.

Direct Unsubsidized Loan

The direct unsubsidized loan is not given based on financial need, but rather to undergraduate or graduate students. This amount is determined by your financial aid advisor based on any other loans you are borrowing and the school’s cost of attendance.

As attractive as this loan sounds, the direct unsubsidized loan will be charged a fixed interest rate from the moment it is issued, until it is the loan is completely paid off. In other words, if the loan is issued in your freshman year of a 4-year college education, the interest will begin to accrue from that moment, throughout all your college years and the entire lifetime of the loan.

However, as of date, the Biden administration has halted federal student loan payments and has kept the interest rate at 0% until September 30th, 2021.

Understanding the differences between the two basic student loans will help you plan out your future finances and capabilities more easily. Remember — you have the choice to reject them if you find that they won’t be appropriate for your situation. Let your college financial aid office know, and they will have to follow your choices.

As we continue into the month of January, there’s no better time than now to revisit the topic of new year’s resolutions. It is common for the start of a new year to present us with a mix of emotions; excitement and anticipation often come with feelings of unease and anxiety. After the champagne is popped and the ball drops, the world holds its breath for the next calendar year to come. New year’s resolutions make their appearance in the collective consciousness, and while last year taught us that plans often fall through, it is human nature to continue striving for excellence and to find the light through difficult times.

The crucial lessons that we learned in staying resilient through the adversities of life means that this year carries the weight of hope, rebuilding, and growth. We hope that this short guide to mindful, soulful, and financial healing will help you build your best resolutions so that you may prosper through 2021 and beyond.

Mindful Healing

As the widely recognized saying goes, “health is wealth.” You don’t need us to remind you of the truth in this statement and that it can be applied to more than just physical health. It is always helpful to keep this motto close to the top of your mind when making even small decisions in your everyday life, which likely still looks like the “new normal” of working and studying from home.

In taking care of your health, your mind should be a top priority. Stress, lack of sleep, and poor diet can keep you from functioning at your full potential. When our minds are tired, it’s difficult to be clear-headed and productive. A clear separation between work and personal life will help you maintain your sanity as stay-at-home orders continue for the time being.

Physically separating work from home can be done by designating work space, and further solidify this by trying to limit your productive hours. It is easy to get caught up in work or school, especially now that it seems to have bled into the home, but making the conscious effort to separate these worlds will help you in the long run by preventing burn-out. In addition, this allows you to take time to focus on personal self-care, such as yoga, meditation, reading, or napping.

In short, treat your mind like a muscle that needs time to rest and recover after moments of strenuous usage.

Soulful Healing

Whether you identify as a spiritual person or not, everyone can find little joys in life that can contribute to soulful healing. Deciding what your soul is seeking this year may require some insightful contemplation, as each person’s soul is unique. For many, this may be taking on a creative hobby such as embroidery, painting, or playing an instrument.

Finding time to engage in self-expression through creation heals the soul, as it is something that you are choosing to do based on your interests and passions alone. There are many resources available online in the form of free and paid courses for nearly any topic you want to try. Any sort of creation is a great way to heal soulfully, even if you don’t see yourself as a creative person. Learning how to cook or bake by trying out recipes online is another fulfilling way to nourish your body and soul.

In a modern world where much of our time is spent working towards career or academic goals, it’s necessary to allocate some parts of your day to creating something just for yourself.

Financial Healing

We get it, talking about money isn’t always comfortable, but it is one of the most common topics when discussing new year’s resolutions. The previous year’s events have affected everyone differently, but what is especially notable is that these events revealed that circumstances can and do change frighteningly fast. We want to balance hope with realistic expectations, and the truth is that we can not expect our lives to shift back to normal anytime soon.

Taking a large financial hit during uncertain times would find anyone anxious, but building healthy foundational knowledge of your financial situation will help. Financial security has always been an issue, now even more so, meaning that it’s important to enter the new year with a plan to ensure your present and future financial livelihood.

If you haven’t already, do your research in order to improve your financial literacy so that you can be informed when you start to map out your finance goals. Some great sources include Refinery29’s Money Diaries, Ellevest Magazine’s Money and Life section, and Tomo Credit’s own blog. Understanding which aspects of your finances you can actually take control of will help you greatly, especially when you start early.

For starters, if you haven’t established a credit score yet, check out Tomo Credit’s zero-interest, no-fee credit card. Since Tomo Credit doesn’t require a previous credit score to apply, this credit card can help you wisely build a good credit reputation with responsible use, helping you grow healthy financial habits. Financial healing starts with reflection, understanding, and planning.

A good credit score is essential for purchasing a new place, a new car, or taking out a loan with better interest rates — but what factors go into the number?

No Single Number

First, there is no definite credit score — there are different credit score models. The credit reporting agencies TransUnion, Experian, and Equifax together give the VantageScore. The FICO score is another well-known and widely accepted model that was introduced in 1989. Creditors use the FICO score to evaluate past credit use for lending decisions.

Factors of the FICO Score

According to the FICO website, the score pulls from five different categories: payment history, amounts owed, length of credit history, new credit, and credit mix.

Payment History (35%)

This is the most important category — it looks at if you have made your credit payments on time. The score in other words reflects your trustworthiness and timeliness. Repeated late payments will damage your score.

Amounts Owed (30%)

This looks at how much of your available credit you are using. By standard, using about 30% is recommended. For example, if you have a $1,000 credit limit, try to use around $300.

Length of Credit History (15%)

This factor looks at how long you have held your credit accounts. The longer, the better — but if you have an old credit account that you have made many late payments on, that will not reflect well on your score.

This category also explains why many people are encouraged to start a credit card as early as possible — especially if you are a college student.

New Credit (10%)

When you open a new credit account, it will decrease your score temporarily, for up to six months. Making new credit accounts however is not discouraged. Rather, you should not be opening too many in a short period of time.

Credit Mix (10%)

The credit mix looks at the different types of accounts you hold: credit cards, loans, and more. Credit cards are considered revolving accounts, where payments are made monthly and are flexible. Installment accounts like mortgage loans are fixed monthly payments. If you prove your responsibility to manage both, it will reflect well on your overall credit score.

The biggest takeaway should be that above all, timely payments are significant in increasing your credit score. You can set up autopay functions like many credit card accounts offer, or set monthly reminders on your phone to manually make the payments.

Although different credit scores have different calculations, these factors overall remain important across the board. Knowing these different factors will help you guide your decisions on credit spending, and opening new accounts.

Traditionally every January, gym sales soar from the wave of new year’s resolutions to exercise — but they quickly decline over the next few months. Relatable, right? However, instead of blaming our own self-will, we can change for the next year by setting new year’s resolutions that have the right balance of ‘realisticness’ and challenge that you can feel better about working towards. After all, the point of a new year’s resolution should be to improve yourself. If you set unreachable goals that you know you will fail at, it will only act as a setback.

Make a Game Plan — by Increments

Start small and set different levels of whatever you want to accomplish. You can set levels according to time. For example, you may start off by going for 1 month of daily exercise. After you’ve achieved that, strive for the next level: another month. This way, you can feel good about yourself for at least reaching the first goal. Additionally, you would feel much less intimidated to work towards smaller goals than a grandiose, almost impossible, goal.

Set Measurable Goals

Creating a vague goal will only deter your efforts to reach your resolutions. Instead, try making them measurable, giving a specific number to your goal. For example, you may write, “Drink 1L of water every day for 1 month.” Or, you may write, “Call family on the 1st of every month in 2021.” This way, not only do you have an exact idea of your plan, but you also have a metric to measure your progress.

Plan Out Your Steps

Once you know your goal, figure out what exactly you need to do to meet that goal. Do you need to set an alarm or reminder on your phone? Do you need to tell your friends and family to keep you accountable? Remember — these steps should be as specific and realistic as possible. The process of creating the game plan itself should feel empowering and more encouraging for you to meet your goals.

Reward Yourself for the Small Steps

In the end, you should feel proud of yourself for at least trying — even if you do not reach your resolution. The effort you put in to at least meet the resolution would have made you a better person than before you tried in the first place. Make sure to remind yourself that your efforts to meet your resolutions are for yourself, and no one else, so there is no need to feel disappointed if those resolutions are not made.

We are currently halfway through December, meaning that the holiday season is in full swing. However, holiday traditions are looking very different this year. Because of travel restrictions and health concerns that are preventing many folks from traveling to see friends and family, this year’s winter festivities may need to be celebrated remotely. While it hasn’t been easy spending nearly a year socially distancing, technological advancements have allowed us to develop creative ways to connect with each other and continue making the best of chaos. To help you have a wonderful holiday and a well-deserved break, we put together this guide to pandemic-safe activities that will put you and your loved ones in the holiday spirit.

Cozy up with hot chocolate

If you’re the type to stay up to date with TikTok trends, you may be familiar with hot chocolate’s latest reincarnation– the hot chocolate bomb. The hot chocolate bomb is not a new delicacy, but has definitely seen an increase in popularity on social media. This classic winter drink received the viral treatment primarily through calming recipe tutorials circulating TikTok. These sweet treats can be bought at local grocery stories, but even better, they are incredibly easy to make at home. Check out this recipe from I Am A Food Blog, and forward it to your loved ones as an invitation to a hot chocolate making session over Zoom or FaceTime.

A new way to enjoy classic holiday films

While nothing may be able to truly replace the feeling of marathoning Christmas movies and being enveloped in warm blankets surrounded by your loved ones, technology can bring us pretty close. Many streaming services don’t allow screen sharing over video conferencing calls, so it takes some creativity and effort to watch movies “together” while socially distant. One way to enjoy films involves trivia games about classic Christmas movies. You can view 99 Christmas trivia questions here, or feel free to have each participant write their own! Another way to enjoy movies is to have a virtual cooking party with recipes from your favorite Christmas films, such as these delicious recipes.

Walking in a winter wonderland

Although the pandemic has put a pause on many in-person activities, there are still ways to get your festive fix. Christmas lights and holiday decorations are abundant this time of year, so put on your walking boots and mask to your nearest holiday location. Walking and viewing beautiful Christmas lights is a great way to relieve stress and remind yourself that the holidays are among us. Enjoy this activity with folks in your bubble or hop on a video call with loved ones to view decorations together.

2020 has been one crazy year, but December has arrived and we’re finally nearing the end of it! Although the holiday season might look a bit different this year, that doesn’t mean you can’t still spread some love and happiness through the act of giving. Finding the perfect holiday gift can be difficult, but that’s why we’re here to give you some ideas and inspiration. We’ve included gift ideas at different price points, so you can choose what best fits your holiday budget!

*Note: Prices may be subject to change.

For the Fitness Fanatics

We all have that one friend who does cardio for fun and eats spinach as a snack (just kidding! Unless…?). Here are some gift ideas for our friend, the wellness guru!

With gyms closing all across the United States, it can be difficult for our fitness friend to get the exercise they need. Ring Fit Adventure can be a nice and fun substitute for those trying to work out at home.

Is today leg day? Wait… leg day was yesterday! What day is it? Sometimes, there can be too many workout plans to keep track of. With a fitness journal, your friend can track their workout routine and their progress!

A BlenderBottle is a great way to make protein shakes on the go. Protein is every fitness fanatic’s bread and butter. BlenderBottles offers a convenient way to make protein shakes and without protein, it can be hard to see results from working out!

For the Pro Gamers

Whether they be a casual gamer or the next eSports competitor, here are some gaming essentials for your gaming friend!

Sitting in front of a screen after hours of playing video games can cause some strain on our eyes. A pair of blue light blocking glasses can help ease eye strain and protect vision.

When playing with friends, communication is key to coordinating strategies or just plain old having a fun time! This HyperX gaming headset will make in-game calls sound high quality. Plus, it looks pretty cool.

For the Beauty Guru

Do you have a friend who always has the perfect contour or diligently follows a 10-step skincare routine? Maybe these gift ideas will be perfect for them!

One can’t have too much makeup, but sometimes it can get a little messy. A makeup organizer will help tidy up anyone’s vanity and make it look clean and put together!

Always remember to wash off all makeup before going to bed — otherwise it could cause unwanted breakouts. Even if you don’t wear makeup, cleansing is super important to wash off all the dirt and oils accumulated throughout the day. A cleansing device can help get rid of all the dirt and grime deep within your skin.

This cat ear hairband not only looks super cute, but is also super practical. Hair can get in the way when applying makeup or washing your face. A hairband will help your hair in place and out of the way.

For the Workaholic

Hopefully, your workaholic friend can catch a break this holiday season. Here are some gift ideas that can help them stay motivated and productive!

Work can get overwhelming with all those deadlines and tasks. Help your workaholic friend stay on track and organized with a new 2021 planner! 2020 was a mess, so let’s leave that behind when we get ready to go into 2021.

The holiday season is a time when all workaholics can finally stop working. It’s time to relax and what better way to relax after a long day of work than with a nice warm bath and a colorful bath bomb?

Coffee is a go-to drink for many workaholics. It tastes good and it keeps you awake during the long hours of work. With a new coffee maker, there will be no more waking up extra early to wait in line at Starbucks before work again!

Gift giving can be a way to show your love and appreciation for a person you care about. Sometimes, finding the perfect gift can be stressful because we all want the receiver to enjoy their gift. With this guide, we hope that gift shopping will be a bit easier this time around. The pandemic forces many of us to celebrate differently this year for the safety of you and everyone else. We encourage you to celebrate while keeping safety guidelines in mind! Doing your holiday shopping early can help beat the crowds and keep yourself safe. Have a great shopping experience and holiday season!

As of November, over 20 million Americans are unemployed and receiving some sort of unemployment benefits. Those are harrowing numbers. With this in mind, nobody’s going to blame you for easing up on gifts this year; times are tough. Meanwhile, you may already be concerned about the state of your savings account. An unexpected bill or emergency car repair can always pop up when you’re the least prepared, that’s why it’s important to have your finances in check this holiday season. Whether you’re barely getting by or need some extra cash for the holidays, here are four ways to keep your finances in order this holiday season:

1. Make a List (and Check it Twice)

If you’re strapped for cash, now would be the perfect time to plan out your holiday budget. Calculate your expenses for the month (rent, insurance, etc.) and set realistic expectations for yourself. Next, estimate how much you will get paid for the month of December (Make sure to include holiday pay and any overtime!). It helps to write all of this information down on paper, or, you could always try using a budgeting app like Mint to track your spending. Now, with your finances tracked, plan accordingly. Maybe you’re all caught up on bills and won’t have to reduce your spending after all. Maybe your finances aren’t looking as healthy as you thought and have to take out a holiday loan. Whatever you do, try not to over do it this year. If 2020 has taught us anything, it’s to expect the unexpected, which in this case, could always manifest itself in the form of unanticipated bills.

2. Get Your Credit in Check

Speaking of bills, there’s no need for your credit card debt to skyrocket this holiday season. You may be considering opening a new credit card for the holidays, I mean, why not right? With retail credit cards, merchants offer heavy discounts on initial purchases and can offer cash back on in-store purchases. On the surface, this may seem like a good way to save money, and it can be! Just be mindful of your credit limits — maxing out your credit card could end up negatively affecting your credit score. In addition to a retail credit card, consider switching to a Tomo Credit Card! A Tomo card is a history-free credit card with flexible limits that will give you 1% cashback on all of your holiday purchases. A Tomo card is also interest free, so you won’t have to worry about any outstanding fees!

3. Try a Side Hustle

There is surely a shortage of side holiday hustles this year as a result of the pandemic, but there are still ways you can manage to make some cash on the side from the comfort of your own home!

Try going through your closet or garage and use a selling app like Mercari. You can sell pretty much anything on the app and now is the perfect time to sell any unwanted clothes or knick-knacks you may have lying around. While you’re at it, try shopping around the app yourself for some deals on Christmas gifts!

If you don’t have anything of value laying around to sell, try browsing through the Nextdoor app. Nextdoor is a community app that functions similarly to Craigslist. People in the community tend to request services in exchange for money such as garden work, pet sitting, tutoring, and more. Otherwise, if you’re more of a creative entrepreneur, I’ve seen people advertising homemade holiday treats and gift baskets up for sale on the app. The best part of the app is that you are only limited to buy and sell within your community, so you won’t have to worry about any shady business deals or scammers.

4. Contactless gift ideas

If Thanksgiving was any indication of what to expect for the holidays, then it’s safe to assume that holiday get-togethers will be kept to an absolute minimum this year. You don’t want your family to risk flying in from abroad, nor do you want to risk any chance of getting your eighty-something year old grandmother sick. Sure, you could always send them a gift in the mail, but in the theme of this year, why not go contactless?

Nowadays, it seems like there’s a subscription box for everything. For Grandma, why not give the gift of knowledge (and caffeine) with My Coffee and Book Club? For Mom, help her save on groceries throughout the year with an Imperfect Foods subscription. For Dad, upgrade his swag with a GQ Best Stuff box. And for your siblings? If they’re of age, they might be delighted with a bottle of wine on their doorstep from Winc every month. But if your siblings are years away from the legal drinking age, then try surprising them with some monthly crafts from KiwiCo. Keep in mind, these are just several ideas out of hundreds of subscription boxes. You’re bound to find something both relevant and within your price range out there.

However you choose to spend your holidays this year, make sure you stay safe and keep healthy! Happy Holidays!

Thanksgiving is right around the corner! Is it your turn to host the Thanksgiving dinner?

Even though Thanksgiving may look slightly different this year, with smaller gatherings and a tighter budget, don’t let that stop you from having a great Thanksgiving meal with your loved ones.

Here are 5 tips on how to prepare the perfect Thanksgiving meal on a budget:

Don’t be a Gordon Ramsay

An amazing Thanksgiving dinner does not have to be extravagant; you won’t need truffle oil or imported saffron. There are a variety of recipes online for budget friendly side dishes that you can create. Don’t forget to check those out! A key tip is that vegetables also tend to be less expensive.

Before heading to the grocery store, make sure you plan out all of the components you will be making. Will you be serving mashed potatoes, pumpkin pie or stuffing? Hopefully it was a yes and a yes. Remember to write a grocery list so you don’t forget anything or get distracted by items you don’t need.

It is crucial to head into shopping season ready to manage spending and your CashScore (CashScore is calculated by your cash inflow and outflow to help you be on top of your hard earned cash!) Here are our tips:

Don’t be afraid to be an extreme couponer

Before heading to the grocery store, check if there are coupons on the groceries that you will be purchasing. When you head to the market, don’t forget to also check the store’s daily specials and coupons. Even if the individual coupons only deduct a small portion from the cost, they will add up. Have you watched Extreme Couponing before? Every cent matters!

Head to the grocery stores early

Not only will there will there be long lines, but also a limited selection of produce left if you decide to shop the day of Thanksgiving. It is important to avoid peak hours in order to stay safe during COVID-19.

Shop early, but not too early. During the week of Thanksgiving, there will be deals on certain items such as Turkey, so you don’t want to miss out on those. Before heading to the grocery store, if you are curious about how busy your local grocery store is, check the grocery store’s location on Google Maps. Under Population Times, there is a live feature where you can view how busy your supermarket is.

Have a Thanksgiving potluck

Make Thanksgiving a collective effort. Delegate dishes to family members and friends. Why make Thanksgiving a stressful experience for yourself when you can relieve the stress by having everyone bring a dish. Your prep and cooking time will also be decreased. Now, you can focus on perfecting your own dish and in return, everyone will bring their best dishes. A potluck will be less expensive for everyone, and everyone gets to participate in the fun of making something. Maybe even make it a friendly competition! Thinking of doing a Thanksgiving potluck now? If so, get your spreadsheet ready!

Most important: Remember it’s about family and friends

Thanksgiving is all about spending time with your loved ones. This year’s Thanksgiving may be especially different, but don’t let that ruin this special time. 2020 has been difficult for many, so remember to cherish this moment with your family and friends.

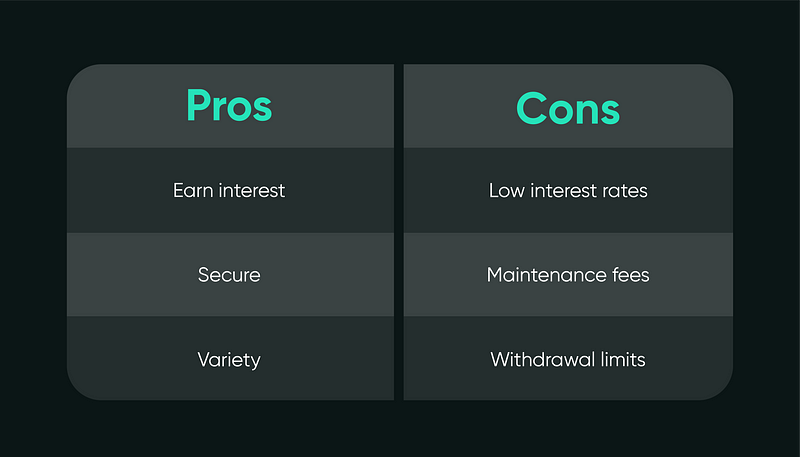

Saving is always wise — but is a savings account the best way to save money?

What is a Savings Account?

While checking accounts are used to store money for daily expenses like food or bills, savings accounts are used to store money over a long period of time. Although fees and withdrawal limits may be drawbacks, savings accounts also offer safety and reliability.

Each type of savings account differs in interest and accessibility, but they generally share these pros and cons:

Pros

Earn Interest

The biggest advantage to savings accounts is that they build interest over time. With your money deposited in their accounts, banks are able to loan money to other customers. Banks return the favor to you by paying interest on the savings accounts. Therefore, the longer you keep the money in your savings account, the more money and the more worthwhile it will be for you. Typically, it’s advised to not touch your savings account as long as possible. Forget about it for some years, don’t do anything, and you’ll earn money.

Secure

If you choose a savings account from a Federal Deposit Insurance Corporation (FDIC) member bank, your account will be insured up to $250,000 under the law. With federal protections, savings accounts are a reliable way to store your emergency funds. To find out if your bank is FDIC-insured, check out FDIC’s Bank Data Guide.

Different Kinds for Different Needs

Besides standard savings accounts, banks are offering more varieties of ways to help you save. High-yield accounts offer higher APY rates compared to basic accounts. The only catch is that you may not be able to access them at bank branches or an ATM. Banks also are offering different types of savings accounts depending on customers’ niche needs. The 529 Plan is tailored for saving for college education costs, offering tax benefits depending on the state you open one in. These specialty accounts all offer interest and security, although they may have stricter restrictions on withdrawals and spending.

Cons

Slow and Low Interest Rates

As much as the idea of earning money while doing nothing sounds attractive, the interest rates are incredibly low. The current national average interest rate according to the FDIC is 0.05% APY. Compared to interest rates of other deposit account options like Certificate of Deposits (CDs) and money market accounts, 0.05% is a very low number. For a full view on national rates on the different kinds of accounts, check out FDIC’s Weekly National Rates and Rate Caps charts.

Fees

To maintain services, banks may ask for a monthly maintenance fee of $4 or $5. In addition, if your funds fall below a minimum requirement, you will be asked to pay fees as well. If you do choose to open a savings account, it is crucial to keep yourself updated on any updated terms and conditions to make sure you avoid fees that may deduct from your earned interest.

Withdrawal Limits

Under the Federal Reserve’s Regulation D, savings account holders are not able to withdraw or transfer funds from their accounts more than six times in a month. This limit allows banks to still reserve some of your deposit and stay in business by using the rest of your money for other services. If you exceed the limit, you may be charged fees, or the Fed may close your account altogether.

However with the widespread impact of the pandemic on individual finances, the Fed lifted the limit on the number of withdrawals and transfers on April 24 to help account holders access their savings and emergency funds.

Main Takeaways

Before opening a savings account, set your personal goals and consider which of the pros and cons matter more to you. There are different kinds of savings accounts, but there are also alternatives to long-term saving rather than opening a basic savings account. You may also look into different kinds of savings accounts and open multiple ones.

This November was reckoned by a chaotic election season that will lead a very unprecedented year, and presidency, to an end. Days after voting, Americans across the country sat in anticipation of the results of a very close presidential race. The suspense built up to a conclusion that found many people unable to hold in their excitement. The announcement of Joe Biden as the winning presidential candidate on November 7th was met with cheers from many who are hopeful for a new beginning that will amend the disorder of 2020 and prior. Whatever your own political preferences may be, it will always benefit you to stay informed about these issues through credible resources.

With urgent matters on the line such as public health, workers rights, and a COVID-19 stimulus bill, the entire country has its eyes trained on the future POTUS, trusting him to make the right choices. From an individual perspective, money is on all of our minds. The question is, how will our personal finances potentially be affected under a Biden presidency?

The Economy at Large

Upon stepping back into the White House, former Vice President Biden will take on a challenge like no other. It is no secret that the economy is continuing to take huge hits during the pandemic as both businesses and their workers are struggling for air. Consumption behaviors have also changed, and the changes may stay long-term as a response to current conditions. While Biden’s predecessor oversaw a pre-pandemic economy that reached historic economic milestones, the current economy is in equally historically worse shape than it started. For now, what we know of Biden’s strategy to tackle this challenge includes a tax policy that will increase taxes on corporations and high-income individuals and other promises for financial relief with individual plans for businesses, unemployed workers, students, and more who were economically affected by the pandemic.

The world rides high on a wave of hope as recent news of a successful COVID-19 vaccine surfaced. After many months in the dark, this news provides a glimmer of hope that also brings to mind Biden’s promise to ensure that once a widely-tested, safe and effective vaccine is available, it will be distributed to every American for free. While these are optimistic notions to hold onto, there are still reparations for financial destruction that must be addressed in the present moment. Shockingly high unemployment levels are still rising, causing concern for long term difficulties among unemployed workers. As the pandemic has revealed disturbing wealth inequalities, Biden is adamant in passing another stimulus bill that would provide eligible Americans at least one more relief check through more direct stimulus payments. Biden’s plan also calls for an additional $200 to monthly Social Security recipients. Apart from individual relief, Biden also outlined plans to provide financial help to small businesses and essential workers.

You can read more about Biden and Harris’s expected COVID-19 action plan here.

Student Debt Forgiveness

Another huge talking point throughout Biden’s campaign involves lessening the heavy burden of student loans off the shoulders of college students everywhere. His loan forgiveness plan includes halving payments on undergraduate federal student loans so that individuals are paying 5% of their discretionary income over $25,000 towards their loans. After 20 years, those who have responsibly made payments through this program will be 100% forgiven for the remaining amount. Individuals with new and existing loans will automatically be enrolled in this income-based repayment program, with the ability to opt-out if they wish. Those making less that $25,000 per year will not owe any payments and won’t accrue interest on undergraduate federal student loans. In addition, Biden is planning on implementing a loan forgiveness program that will offer $10,000 of undergraduate student debt relief for every year of national or community service for up to 5 years.