Credit card debt, or any debt for that matter, can be a huge headache. No one likes to borrow money, especially if there is interest accruing on top of that. This New Year, make sure you are well organized and have a plan focused on your financial goals. SF based startup, TomoCredit, helps their users manage credit debt through one of their unique card features — weekly autopay. Users don’t have to worry about remembering to pay on time or carrying a large balance. Instead, the autopay feature triggers weekly on users’ full balance. This means a quicker credit score boost AND 0 credit debt! You start with a 0 balance every week.

Nothing says “new year, new me” like a freshly paid-off credit card every week! Asides from the nifty autopay feature, TomoCredit also features a 0% APR/0 interest AND you don’t have to have credit history to apply!

A good credit score is essential for purchasing a new place, a new car, or taking out a loan with better interest rates — but what factors go into the number?

No Single Number

First, there is no definite credit score — there are different credit score models. The credit reporting agencies TransUnion, Experian, and Equifax together give the VantageScore. The FICO score is another well-known and widely accepted model that was introduced in 1989. Creditors use the FICO score to evaluate past credit use for lending decisions.

Factors of the FICO Score

According to the FICO website, the score pulls from five different categories: payment history, amounts owed, length of credit history, new credit, and credit mix.

Payment History (35%)

This is the most important category — it looks at if you have made your credit payments on time. The score in other words reflects your trustworthiness and timeliness. Repeated late payments will damage your score.

Amounts Owed (30%)

This looks at how much of your available credit you are using. By standard, using about 30% is recommended. For example, if you have a $1,000 credit limit, try to use around $300.

Length of Credit History (15%)

This factor looks at how long you have held your credit accounts. The longer, the better — but if you have an old credit account that you have made many late payments on, that will not reflect well on your score.

This category also explains why many people are encouraged to start a credit card as early as possible — especially if you are a college student.

New Credit (10%)

When you open a new credit account, it will decrease your score temporarily, for up to six months. Making new credit accounts however is not discouraged. Rather, you should not be opening too many in a short period of time.

Credit Mix (10%)

The credit mix looks at the different types of accounts you hold: credit cards, loans, and more. Credit cards are considered revolving accounts, where payments are made monthly and are flexible. Installment accounts like mortgage loans are fixed monthly payments. If you prove your responsibility to manage both, it will reflect well on your overall credit score.

The biggest takeaway should be that above all, timely payments are significant in increasing your credit score. You can set up autopay functions like many credit card accounts offer, or set monthly reminders on your phone to manually make the payments.

Although different credit scores have different calculations, these factors overall remain important across the board. Knowing these different factors will help you guide your decisions on credit spending, and opening new accounts.

This pandemic has no doubt been hectic for everybody. With millions of Americans losing their jobs, millions unemployed, and millions infected, millions of us are growing more and more frustrated. When the shelter-in-place orders began back in March, like most of you, we were worried about what the future would hold for us. As most of you know, working remotely presents its challenges. But we are reorganizing and getting back on track. We just wanted to take the time to write this to let you know that…

We Hear You

We have received countless inquiries about the Tomo waitlist and rightfully so. An overwhelming amount of you have been waiting for your card for months at this point, and we understand your frustration. As of now, we have over 100,000 people on the waitlist. Due to some changes related to the pandemic, we currently process all of our pre-approvals manually. The moment they are processed, we send out invites in waves and, thankfully, we will be sending out an increasing number of waves in the coming months. We recommend that over the course of these next few months that you keep an eye out for your invite. If you don’t receive an invite by then, please reach out to us. We are in the process of reorganizing our customer support and will be adequately prepared to answer any questions you may have for us moving forward. However, due to the volume of applications we have received, please keep in mind that we will be prioritizing the questions of current cardholders first.

We know that sounds like a long time, but it will be worth it. Trust us. We have big plans for the future here at Tomo!

What’s Changing

Since the pandemic provided some unpredictable challenges, our credit card has had to make some fundamental readjustments. With a heavy heart, we must eliminate the Tomo Credit Card “2 for 2” cash back referral perk. We hope to be able to deliver you other more unique and personalized rewards in place of the “2 for 2” referral program, and we intend to work with merchants in order to create a user experience that you’d expect from “the credit card of tomorrow”. Don’t worry, you will still receive 1% cashback on all purchases and we will continue to offer you a history-free credit card with flexible limits and no hidden fees. Our goal here at Tomo has always been to help our members establish the financial security they deserve, not to profit off of their financial insecurity like the big banks do. For those of you that have referred members to tomo, fear not, as our new referral program will be released in the near future and you will still be awarded for those referrals.

We can also offer one other awesome perk to you should you meet the requirements, and that’s up to 20% cashback. Yeah, you read the right. 20%. If 20% cashback is what you desire and you think you’re qualified, we encourage you to apply to become a Tomo ambassador! As ambassador, you will promote the Tomo card and encourage your community to sign up for one via a personalized referral code. For each person you refer that gets approved, you will receive an additional 1% cash back, with a maximum cap of 20%. That means that if you get 20 people to sign up, you’ll get that sweet 20%. Keep in mind though that the ambassador cashback bonus is valid for 3 months from the time each of your referrals is approved. Think you can do it? Apply to become an ambassador here!

What’s in Store

We cannot thank our members enough for their overwhelming support. Tomo has always believed that you are worth more than an arbitrary credit score. We have always been dedicated to helping our members build credit and save money, and, moving forward, we hope to win back your trust. As we proceed, we will be making adjustments to our card in order to better cater to our members’ needs.

But first things first: I think that we can all agree that this year has just got to end already. When the pandemic begins to slow down, we promise to speed things up, and to be more prepared than ever to provide you with the experience you deserve from the credit card of tomorrow.

For many college students, student loans are a major component in helping to afford college. Life after college can be especially confusing when having to manage both student loans and personal finances. For some, it is the first time they have to deal with things like budgeting and making student loan payments. Many schools also do not teach financial literacy, leading there to be several common misconceptions regarding student loans and credit score. So, how does student loan affect credit score?

Many believe that there may be a good or bad association between student loans and credit score, or that there is no relationship at all. But in reality, student loans can affect your credit score both negatively and positively.

How to avoid student loans from hurting your credit score

There are five components that make up your credit score: amounts owed, new credit, payment history, credit mix, and length of credit history. Student loans affect payment history, credit mix, and length of credit history.

Keeping up with monthly payments is key. Payment history makes up 35% of your credit score. While forgetfulness does occur, missing continuous payments will be detrimental to your payment history. Payments that are overdue should be taken care of immediately. The more overdue your payment is, the larger the consequence that you will face. You may end up going into default as a result. For federal student loans, this occurs after 270 days of not making the payment, and for private student loans this occurs after three months. Your credit score will drop when your lender reports the late payment to one or all of the three major credit bureaus.

Remember to borrow mindfully. Applying for new loans can hurt your credit score, especially if you have several loans, do not have a long credit history, or student loans are your only form of credit.

If you are forgetful, it may be helpful to schedule reminders on your calendar or set up autopay. If you cannot pay your student loans, try asking your lender to pause or lower your monthly student loan payments as soon as possible.

How credit can benefit your credit score

Conversely, making payments on time will improve your payment history, and therefore benefit your credit score. Presumably, if you have student loans, you will be repaying it within several years. The amount of time taken to repay your student loans affects your length of credit history. Having a history of making regular payments will present you as a reliable borrower to lenders. Student loans also help to diversify your credit mix, increasing your credit score.

If you have student loans, it is important to stay informed about their effects on credit score. How student loans affect your credit score will depend on how you manage your student loans. Making sure to stay organized and on top of your payments will lead you to a better credit score. Having a good credit score is vital to your financial health. You will receive many benefits from a good credit score including low interest rates on credit cards and loans, a higher chance for loan approvals, and much more. If you would like to improve your credit score, consider applying to Tomo. No credit history required, no interests or fees, and your credit will never be pulled.

Do you really need that extra piece of plastic in your wallet? Yes, and here’s why.

Build credit.

A credit score and credit history may seem ambiguous now, but there will come a day when you will wish for that high credit score and long credit history. Whether it is renting or buying a property or financing a car purchase or some other large purchase, your credit score and credit history matter. They will determine if you get approved for that new home or new car, and the borrowing rate you are charged. Would you rather pay more than necessary? Absolutely not, no one does. Time to get a credit card and start building that credit.

Rewards.

There are so many credit cards out there and most of them offer some form of rewards, sometimes even just for signing up! Besides sign-up bonuses, most credit cards offer continuous cash back rewards as you use the card. Why not start paying yourself back for spending money?

Interest-free borrowing.

By using credit cards, you can borrow money for a short period of time and pay zero interest as long as you pay off the credit card in full by the payment due date. You can’t get a lower rate than that.

Peace of mind.

Most credit cards come with some form of insurance these days. This means if you have a fraudulent charge on your card, you can easily report it to your bank and get the funds back right away. If you rely on using cash for all transactions, you risk getting it stolen or simply losing it. With a debit card, your money actually leaves your bank account if a fraudulent charge were to occur. You will eventually get your money back, but it can take longer than if it were to happen to a credit card.

Avoid foreign transaction fees.

There is a lot of world to see and that requires traveling. If you get the right credit card, you can avoid foreign transaction fees when traveling in a different country, which can add up quickly. Save your money for traveling and don’t waste it on fees.

Convinced you need a credit card now?

Be one of the first to get in on the next generation of credit cards. Visit TomoCredit.com to learn more.

I recently moved to San Francisco from London to study for an MBA at Berkeley Haas because I wanted to be at the heart of the tech ecosystem and learn more about the innovation happening within financial services. In order to understand this landscape more, I wanted to work with a company innovating the space, and I’m lucky enough to be working with Tomo.

Tomo addresses a huge pain point I had when I moved here as an international, a lack of US credit history. A lack of credit history meant I was unable to apply for almost all credit cards and unable to earn a variety of rewards offered by different card companies. Additionally, credit history is a requirement for some cell phone plans, for apartment rental eligibility and it can have an adverse impact on the amount you pay for insurance premiums. However, through lots of market research for an alternative and for interesting Haas affiliated fintech companies, I came across Tomo which was tackling both of these issues.

Tomo is a fintech startup that currently offers a credit card that does NOT require you to have a credit score, which is exactly what I was looking for. I reached out to the founder Kristy and was able to get an early look at the product and the functionality they are offering. They are also working on technology that allows you to get approved for a card without having an SSN which is how I was able to get a card. This is a game-changer for international students who often have no credit history or SSN.

Me with my Tomo card!

Not only did they get me my first credit card, but they also offer crazy cashback! For every person you refer and is approved, you will EACH receive an additional 1% in cashback which is how in a short amount of time I’m earning 8% cashback! You can do this with up to 19 people at a time allowing you to boost your cashback up to 20%. Whilst doing all of this, I am building up my credit history! It’s honestly amazing.

There is limited availability and the waitlist is filling up fast. So if you are looking for a modern-day credit card with the best cashback or you have no credit score or SSN, then Tomo is the card for you!

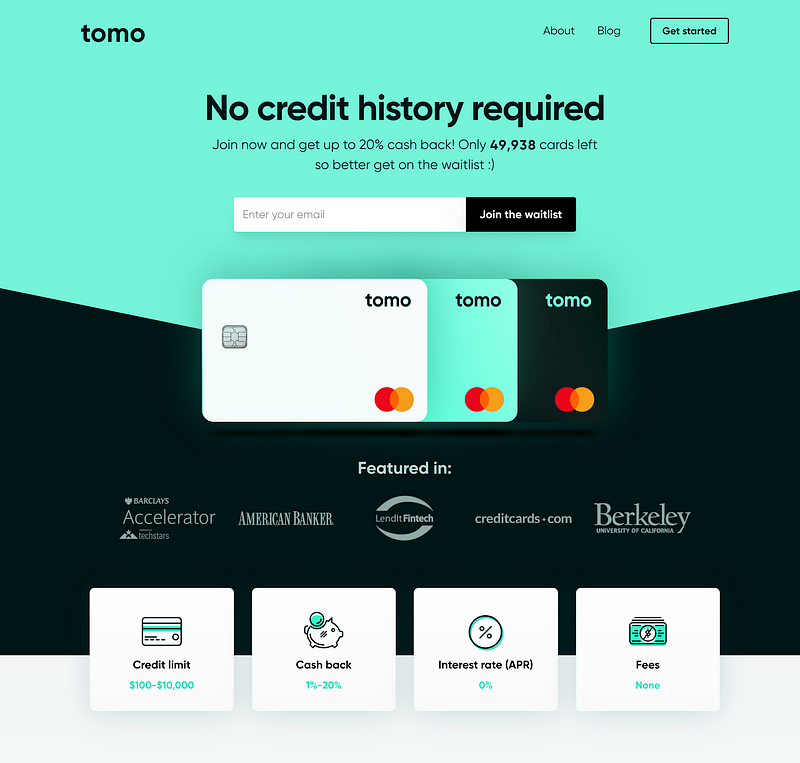

Here at Tomo, we know you’re not just a credit score. When you sign up today not only can you get approved with no credit history but we are the first card offering up to 20% in cashback. EVER.

How does it work?

First, you’ll want to sign up for our waitlist. When you get your welcome email, simply apply for our card like you would for any other credit card — minus the credit check! Tomo Credit assesses your eligibility not by looking at your credit score, but by analyzing your banking history.

Once accepted you will receive a unique referral code that you can share with your friends, colleagues and acquaintances. For each person that is approved for a card, you both receive 1% in cashback rewards.

Cashback works via redeeming the Tomo points you earn from spending on your Tomo card for cash. For example, if you have referred 19 people that get approved for a Tomo card, you will earn 20% in cashback. When you spend $100, you will receive 2,000 points. 100 Tomo points = $1 in cash so the 2,000 Tomo points you earned are worth $20 in cash which can be withdrawn into your checking account. It’s that simple.

Your cashback bonuses for referring people are valid for three months and you can replenish these with new referrals to keep your cashback high for a longer period.

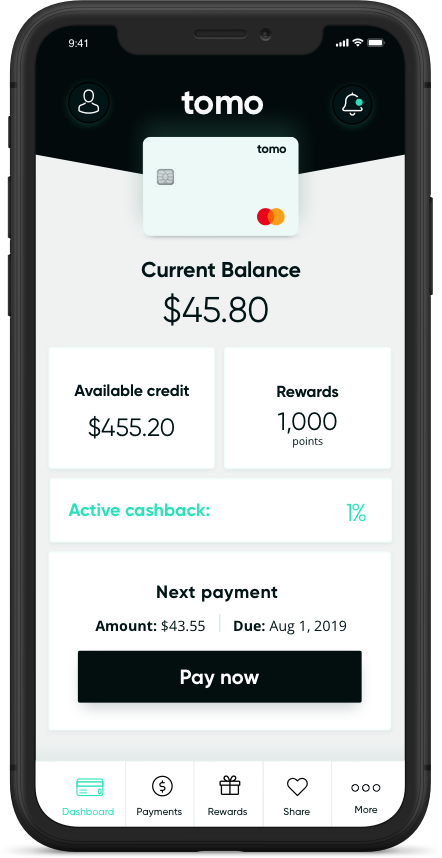

You can track your balance, rewards, and pay off your card on the dashboard on mobile or web browser.

Tomo cards are currently limited to only 50,000 so the quicker you sign up the better. Also, don’t forget the more you share, the more rewards you will earn!

You can get on the waitlist by using the below link:

For better or worse, one of the most important metrics in your financial life is your credit score. Most Americans aren’t well informed of this in their traditional upbringing and as a result are left playing catch-up later in life or simply don’t understand some of the core benefits of having a high credit score.

This 3-digit number can either cost you or save you hundreds of thousands of dollars over the course of your lifetime and the sooner you can get ahead of it the more beneficial it will be for your life.

Here are 5 of the best ways we at TomoCredit recommend to best improve your credit score

Create accounts and monitor your credit scores frequently

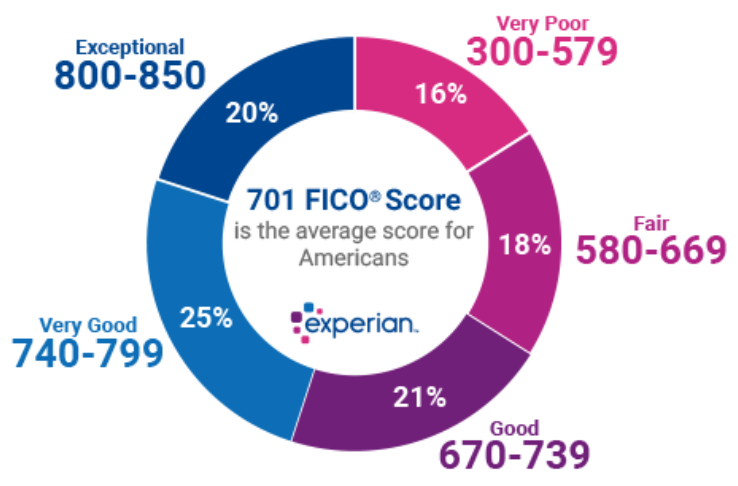

Improving your credit score starts with knowing what it exactly is. We recommend creating accounts on at least two of the major credit card portals including Credit Karma, Credit Sesame, Credit.com, Quizzle, and WalletHub. You can also create an account on AnnualCreditReport.com where you can check your credit report for free once every 12 months from each of the major credit bureaus — Equifax, Experian, and TransUnion. See the below graph (from Experian) for an idea of what the average American credit score is and what ranges are considered good — bad scores.

Get this tattooed, carve it in stone, or repeat it over and over again until it’s memorized. This is probably the easiest way for an individual to steadily build their credit score over time but is also the most abused. It’s simple and straightforward yet millions of Americans take liberties with their credit card spending and let their credit payments carry over consecutive months and damaging their credit scores. Inherently credit scores are a reflection of your ability to pay off debts over time signaling your reliability. You can positively influence this indicator by using calendar reminders or setting your bills on auto-pay to help ensure you pay on time every month. Paying your bills late or settling your debts for less than what you agreed on will negatively affect your score.

3. Keep your balances low

An important part of today’s credit scoring systems is your credit utilization ratio. This ratio is calculated by looking at the credit balances you have across all your cards at a given time and dividing that by the total credit limit you have across all of your credit cards. What you are left with is a ratio that has a significant weight to your total credit score. Lenders look for credit ratios of 30% or less, so your credit utilization ratio should fall below this number in order for it to have a positive impact on your score. Example: if you typically have $1k a month in credit balances and your total credit limit across your cards is $5k then your credit ratio is 20%.

Best way to improve your credit utilization ratio, and as a result your credit score, is to keep your overall balances low! On this note if you have unused cards we recommend not closing these accounts as long as you aren’t paying costly fees. The additional credit limits will help your credit utilization ratio as long as you keep the account open but just don’t spend on them.

4. Avoid too many hard credit inquiries and don’t open more accounts than you need

Applying for loans or new credit cards will result in hard inquiries which can take a negative toll on your credit score and remain on your record for 2 years. This can ultimately be mitigated over time but requires careful overview. If you already have cards open be smart about which accounts you utilize and avoid closing credit lines if you don’t need to. At the same time however don’t open new credit cards if you don’t need them and put your spending habits at risk.

5. Start building and proactively maintaining your credit score as early as possible

The toughest part of starting to build your credit history is not having one at all. At some point you’ll need to qualify for a credit card and start building up a balance with regular payments to show future creditors and lenders that you are a trustworthy borrower. Not many cards will take chances on immigrants or even young professionals. This is where we at TomoCredit hope to help empower folks towards building a healthier credit history. Our card uses alternative evaluation methods compared to traditional card providers to ensure that you can get a card that will serve you with high rewards and put you on the path to financial success.