As we continue into the month of January, there’s no better time than now to revisit the topic of new year’s resolutions. It is common for the start of a new year to present us with a mix of emotions; excitement and anticipation often come with feelings of unease and anxiety. After the champagne is popped and the ball drops, the world holds its breath for the next calendar year to come. New year’s resolutions make their appearance in the collective consciousness, and while last year taught us that plans often fall through, it is human nature to continue striving for excellence and to find the light through difficult times.

The crucial lessons that we learned in staying resilient through the adversities of life means that this year carries the weight of hope, rebuilding, and growth. We hope that this short guide to mindful, soulful, and financial healing will help you build your best resolutions so that you may prosper through 2021 and beyond.

Mindful Healing

As the widely recognized saying goes, “health is wealth.” You don’t need us to remind you of the truth in this statement and that it can be applied to more than just physical health. It is always helpful to keep this motto close to the top of your mind when making even small decisions in your everyday life, which likely still looks like the “new normal” of working and studying from home.

In taking care of your health, your mind should be a top priority. Stress, lack of sleep, and poor diet can keep you from functioning at your full potential. When our minds are tired, it’s difficult to be clear-headed and productive. A clear separation between work and personal life will help you maintain your sanity as stay-at-home orders continue for the time being.

Physically separating work from home can be done by designating work space, and further solidify this by trying to limit your productive hours. It is easy to get caught up in work or school, especially now that it seems to have bled into the home, but making the conscious effort to separate these worlds will help you in the long run by preventing burn-out. In addition, this allows you to take time to focus on personal self-care, such as yoga, meditation, reading, or napping.

In short, treat your mind like a muscle that needs time to rest and recover after moments of strenuous usage.

Soulful Healing

Whether you identify as a spiritual person or not, everyone can find little joys in life that can contribute to soulful healing. Deciding what your soul is seeking this year may require some insightful contemplation, as each person’s soul is unique. For many, this may be taking on a creative hobby such as embroidery, painting, or playing an instrument.

Finding time to engage in self-expression through creation heals the soul, as it is something that you are choosing to do based on your interests and passions alone. There are many resources available online in the form of free and paid courses for nearly any topic you want to try. Any sort of creation is a great way to heal soulfully, even if you don’t see yourself as a creative person. Learning how to cook or bake by trying out recipes online is another fulfilling way to nourish your body and soul.

In a modern world where much of our time is spent working towards career or academic goals, it’s necessary to allocate some parts of your day to creating something just for yourself.

Financial Healing

We get it, talking about money isn’t always comfortable, but it is one of the most common topics when discussing new year’s resolutions. The previous year’s events have affected everyone differently, but what is especially notable is that these events revealed that circumstances can and do change frighteningly fast. We want to balance hope with realistic expectations, and the truth is that we can not expect our lives to shift back to normal anytime soon.

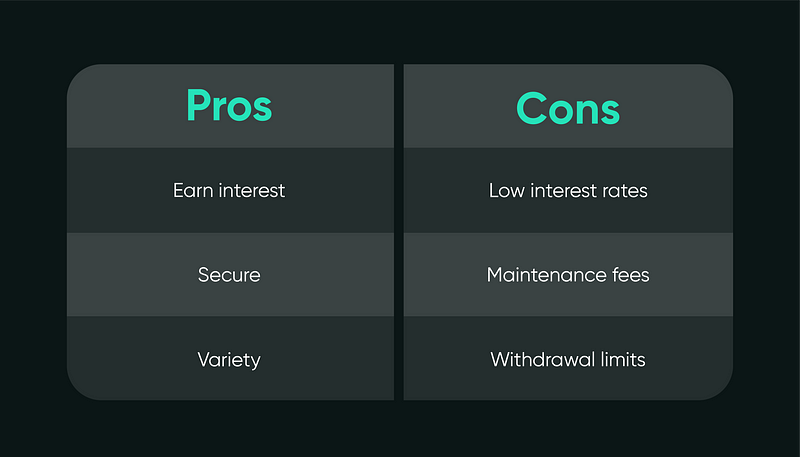

Taking a large financial hit during uncertain times would find anyone anxious, but building healthy foundational knowledge of your financial situation will help. Financial security has always been an issue, now even more so, meaning that it’s important to enter the new year with a plan to ensure your present and future financial livelihood.

If you haven’t already, do your research in order to improve your financial literacy so that you can be informed when you start to map out your finance goals. Some great sources include Refinery29’s Money Diaries, Ellevest Magazine’s Money and Life section, and Tomo Credit’s own blog. Understanding which aspects of your finances you can actually take control of will help you greatly, especially when you start early.

For starters, if you haven’t established a credit score yet, check out Tomo Credit’s zero-interest, no-fee credit card. Since Tomo Credit doesn’t require a previous credit score to apply, this credit card can help you wisely build a good credit reputation with responsible use, helping you grow healthy financial habits. Financial healing starts with reflection, understanding, and planning.