According to Bankrate, 46% of credit card holders are currently carrying debt month-to-month due to inflation and paying for daily expenses. 50% of GenZ don’t know and don’t understand the APR linked to their debt. So what does this mean?

With no real idea of when inflation will start to go down, many young adults are relying on their credit cards to make purchases. What many of them do not understand is how carrying a balance can affect their credit score and the impacts of interest rates on their balance.

By carrying debt and not being able to pay back, people are racking up fees from the high interest rates and negatively impacting their credit scores. In a survey from Bankrate that asked which credit card feature is the best and most often used, 36% answered cash back rewards. Cashback is great, BUT, it can be more of a short-term strategy to pay down debt. Instead of thinking about immediate returns, young adults should start strategizing a plan for longer-term debt payoff, like choosing credit cards with 0 or low APR.

Enter Tomo, 0% APR/interest credit card that doesn’t require credit history. The Tomo card, also known as GenZ’s favorite credit card, has gained popularity among young adults due to its 0 APR and ability for card holders to never carry a balance. This is the perfect card in 2023 as more and more Americans are leaning on credit cards to pay off daily expenses.

If you suffer from a low or (in many cases) no credit score, it may be quite difficult to achieve some of your personal financial goals. Some of these goals include: obtaining an auto loan, mortgage, or applying for any other types of loans.

According to FICO’s most recent statistics, only 1.6% of 232 million U.S. consumers have a perfect credit score at 850. This feat may seem unachievable, but it isn’t impossible.

We surveyed 100 people in San Francisco and asked them what their credit score is. Many answered in the mid-600s to 700 range, with a handful above 800 and some at a PERFECT 850.

We asked those that were above 800 how they achieved this. The following are some tips and tricks they shared:

Pay your bills on time and always pay over the minimum.

Don’t max out your cards.

Keep a low or 0 balance. Some companies, like TomoCredit, feature autopay, so you never have to worry about making a late payment. Tomo’s autopay triggers weekly, so you’ll also never keep a balance.

Only spend on what you need, not what you want.

Have a budget and stick to it. Seems simple, but can be difficult and challenging in practice.

Create a strategy for your credit card usage — designate a credit card to the spending type. For example, if you have more than one credit card, use one for gas and groceries only and the other for major purchases.

Don’t open too many accounts. Retail stores usually have people fall prey to their credit card programs and many tend to forget they signed up for the card until they receive a late payment notice in the mail.

Understand your APR/interest rates. Know how much you are paying and what you will need to pay.

Don’t close your credit card accounts. This factors into your FICO on credit card length history.

Check your score for free. Experian, Transunion, Equifax all have annual free credit reports. Some of your current accounts may also show you your current score on the dashboard when you log in, like Tomo’s dashboard for instance.

It’s 2023 and you’ve finally decided to open a credit card. Congrats and welcome to the credit building family! We’re so proud of you for taking action towards your personal financial journey 🙂

TomoCredit wants to share with you 6 tips that will help you maximize your Tomo card:

1. Pay your bills on time. Luckily, the TomoCard has a weekly autopay feature that allows you to build credit with ease. No need to remember to pay your bills and risk late fees, we got you!

2. Check your credit score. The Tomo app dashboard displays your credit score as soon as you log into your account. We want to make it easy and convenient for you to understand your credit building journey.

3. Pay the full balance/keep balances low. Try not to keep a balance on your credit card and try to maintain a low or 0 balance. This will help build your credit fast and document healthy spending habits. With Tomo, you will never hold a balance, since our card triggers weekly autopay on the full balance.

4. Monitor fraud charges! Always make sure to keep an eye on your account and check frequently for any errors of fraudulent charges. The New Year typically brings in good deals for savings, requiring personal information and payment methods. Make sure that you are diligent and pay attention to where you shop and give your money to.

5. Be strategic with your credit card. For first time credit card holders, a good tip would be to use the card for one bucket, so you know exactly where your money is going and how much to expect when you spend. For example, delegating the card to use for groceries and gas only, or subscriptions like Netflix/Hulu only. This makes it easier for you to keep track of your spending while easily boosting your credit score.

6. Use your perks! Many people forget to take advantage of all the benefits and services that their credit cards offer. TomoCredit card is among many that offer great benefits for its members. Because Tomo is partnered with MasterCard, we offer World Elite Benefits, which include:

Cell Phone Protection: Pay your cell phone bill with your Tomo Card and you’re protected for up to $1,000 against damage or theft.

Zero Liability Protection: As a Mastercard cardholder, you’re not responsible in the event that someone makes unauthorized purchases with your card.

Mastercard Global Service: Get emergency assistance and in any language. Also helps with reporting a lost or stolen card, obtaining an emergency card replacement or cash advance, finding an ATM and answering questions on your account.

Mastercard ID Theft Protection: Activate your card by registering your card number and receive alerts when suspicious activity is detected and resolutions services if needed.

DoorDash: Cardholders that are new to DashPass will receive a three-month membership. Cardholders will also get a $5 discount on their first order each month (valid until September 30, 2023 or while supplies last) — this $5 discount requires having a DashPass membership.

Lyft: Get a $5 credit for every three rides taken in a calendar month (capped at one per month).

HelloFresh: Get 5% back on each HelloFresh purchase that can be used towards a future HelloFresh order.

ShopRunner Membership: Get free two-day shipping and free return shipping at over a hundred online retailers.

Fandango Credit: Get $5 off your next purchase when you spend at least $20 on movie tickets or streaming with Fandango.

World Elite Concierge: 24/7 access to a concierge service that can help you with tasks such as obtaining hard-to-find event tickets.

Hope these tips were helpful! To apply to the TomoCard, check out our website: www.tomocredit.com.

BNPL has taken consumers by storm in the last few years. But these apps, like Klarna, Afterpay, etc. should not be expecting the same results from spenders in 2023.

Consumers this new year are much more diligent and smart with how they spend their money. With more tools and education on financial literacy and startups, like TomoCredit, placing the importance on smart spending, consumers are all ears (especially in this economy).

Consumers are finally being hit with the high interest they spent on their electronic devices from last holiday. They are learning from their mistakes and to not “bite on an easy hook.”

SF based startup, TomoCredit, announced that they’ve seen a huge spike in applications in 2022 because of their no interest/0 APR card feature. CEO and founder, Kristy Kim, explains that consumers are feeling the aftermath of easy spending with BNPL options, but don’t understand the repercussions until they see interest fees charged to their account.

As many of us are planning our New Year’s Resolutions, it seems safe to say that Financial Resolutions usually make the top of the list.

This year, TomoCredit, an SF based startup, wants to help millions reach their highest credit score, as FAST as possible. TomoCredit is targeted towards GenZ and Millenials and aimed at helping those who don’t have any credit history/bad credit.

The TomoCard has some unique features that make it the best credit card of 2023 to help build credit fast. Here are 5 key features:

Weekly Autopay — this means on-time payments and 0 balance every week. Because of the weekly payoff, your healthy spending habits are being reported more frequently to all 3 credit bureaus (Experian, Equifax, TransUnion). Frequent reporting = credit building FASTER.

0% APR/interest — yes, you read that right

Up to $10,000 credit limit

SSN not required to apply!

Free benefits worth over $500!

So, what are you waiting for? Start your 2023 with Tomo.

This New Year, TomoCredit, a fintech startup based out of San Francisco, CA, wants to help you build credit even if you don’t have a credit history! (or if you simply need to rebuild your score).

The Tomo card, better known as “GenZ’s favorite credit card”, lets you build credit without having ANY credit history. The card also has 0% APR/interest and since it is MasterCard “World Elite,” there are a ton of perks for members, including: $1000 cell phone protection and Lyft/DoorDash/HelloFresh credits. Talk about a win-win!

The Tomo card also features weekly autopay, which allows users to boost their credit FAST. What better way to start the New Year than with good credit?! The Tomo card reports to all 3 credit bureaus — Equifax, Transunion, and Expedia.

So if you plan on buying a home, car, or any other expense requiring a loan, this card will help you reach your credit score goals.

Check out how we are on a mission to help millions of others reach their financial and credit score goals by visiting our website: tomocredit.com

Time management is something we could all get better at, let’s be honest. Whether it be on the job, in school, or even in your personal life, effective time management has significant benefits. Time management helps you accomplish more tasks quickly and leaves you stress free. There are many different ways to go about managing your time and tools to help you get started, making this much easier. The downside of this is that it can sometimes feel like there are too many different apps out there. Luckily, there are only a few you actually need to tackle time management head on.

Download a Calendar App

One of the most important tools, if not the most important, you can use is a calendar app. A good calendar app will allow you to use it with several devices including your mobile phone and computer. This way, you will always have your calendar right at your fingertips and be able to quickly add something without giving it a second thought or wasting a second of your time. An app likse Google Calendar can not only sync any changes made from multiple devices, but can remind you of upcoming events, allow you to share events with friends, or create a Google Meet call with the touch of a button. These help you to do more and be more connected, especially via Google Meet (a major selling point when working from home or socially distancing).

Make a To-Do List

Another classic time management tool is a to-do list. Although pretty old-fashioned, this tried and true method holds you accountable for all you need to accomplish on any given day. The key to success is not falling behind and setting realistic goals. No, you probably can’t get everything you need to get done before November in the next 3 days, but you can certainly get everything you need done today ahead of time and set yourself up for success. If you end up falling short of your goal, don’t give up. Instead, restructure your list so it’s a bit more realistic and try again tomorrow. By keeping your daily to-do lists short enough to be achievable, you will not only be on track to complete everything you need to get done ahead of time, but you might even end up having fun doing it and want to knock some things off tomorrow’s list as well. Don’t believe it? Try it yourself!

Clean Out Your Inbox

Lastly, take the time to clean out your email inbox. It’s not fun, but by unsubscribing to all the emails you no longer wish to receive and deleting old ones, you’ll find yourself spending much less time sifting through your entire inbox of 11,479 unread emails. As an added bonus, you won’t miss any important events or news you might need to attend to.

Benefits

These methods can help you get more tasks accomplished faster. As if that wasn’t good enough, you’ll soon find yourself having more free time on your hands after getting things done ahead of time. Say goodbye to the stress of having too many things to do and not enough time. You’ll no longer need to bear the weight of knowing you should have done more today or that you’ll have to pick up the slack tomorrow.

The benefits of good time management are linked to financial health — often overlooked but necessary to achieving the things you want faster. Both time and money are necessary commodities that will enhance your life when managed mindfully. With good financial health, you will be better positioned to achieve more of what you want in life.. For example, you’ll be eligible for better mortgages, auto loans, and many other things! These will all save you a ton of money over the course of your lifetime. By continually saving, you’ll save yourself the worry of being unable to tap into your emergency fund should a major crisis come your way.

For better or worse, one of the most important metrics in your financial life is your credit score. Most Americans aren’t well informed of this in their traditional upbringing and as a result are left playing catch-up later in life or simply don’t understand some of the core benefits of having a high credit score.

This 3-digit number can either cost you or save you hundreds of thousands of dollars over the course of your lifetime and the sooner you can get ahead of it the more beneficial it will be for your life.

Here are 5 of the best ways we at TomoCredit recommend to best improve your credit score

Create accounts and monitor your credit scores frequently

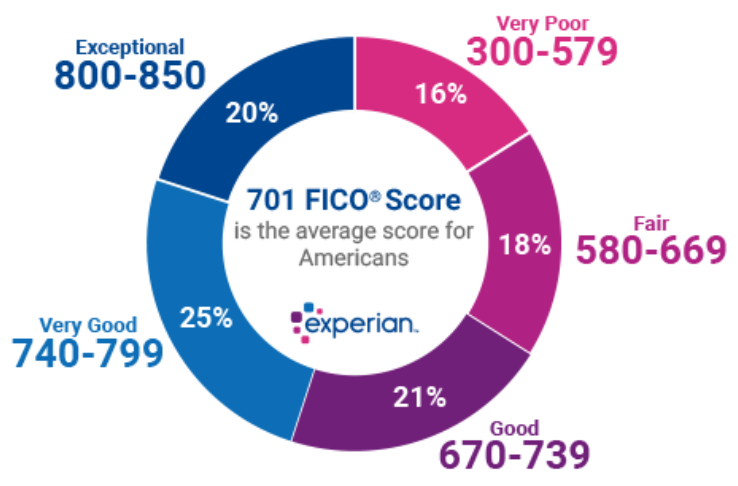

Improving your credit score starts with knowing what it exactly is. We recommend creating accounts on at least two of the major credit card portals including Credit Karma, Credit Sesame, Credit.com, Quizzle, and WalletHub. You can also create an account on AnnualCreditReport.com where you can check your credit report for free once every 12 months from each of the major credit bureaus — Equifax, Experian, and TransUnion. See the below graph (from Experian) for an idea of what the average American credit score is and what ranges are considered good — bad scores.

Get this tattooed, carve it in stone, or repeat it over and over again until it’s memorized. This is probably the easiest way for an individual to steadily build their credit score over time but is also the most abused. It’s simple and straightforward yet millions of Americans take liberties with their credit card spending and let their credit payments carry over consecutive months and damaging their credit scores. Inherently credit scores are a reflection of your ability to pay off debts over time signaling your reliability. You can positively influence this indicator by using calendar reminders or setting your bills on auto-pay to help ensure you pay on time every month. Paying your bills late or settling your debts for less than what you agreed on will negatively affect your score.

3. Keep your balances low

An important part of today’s credit scoring systems is your credit utilization ratio. This ratio is calculated by looking at the credit balances you have across all your cards at a given time and dividing that by the total credit limit you have across all of your credit cards. What you are left with is a ratio that has a significant weight to your total credit score. Lenders look for credit ratios of 30% or less, so your credit utilization ratio should fall below this number in order for it to have a positive impact on your score. Example: if you typically have $1k a month in credit balances and your total credit limit across your cards is $5k then your credit ratio is 20%.

Best way to improve your credit utilization ratio, and as a result your credit score, is to keep your overall balances low! On this note if you have unused cards we recommend not closing these accounts as long as you aren’t paying costly fees. The additional credit limits will help your credit utilization ratio as long as you keep the account open but just don’t spend on them.

4. Avoid too many hard credit inquiries and don’t open more accounts than you need

Applying for loans or new credit cards will result in hard inquiries which can take a negative toll on your credit score and remain on your record for 2 years. This can ultimately be mitigated over time but requires careful overview. If you already have cards open be smart about which accounts you utilize and avoid closing credit lines if you don’t need to. At the same time however don’t open new credit cards if you don’t need them and put your spending habits at risk.

5. Start building and proactively maintaining your credit score as early as possible

The toughest part of starting to build your credit history is not having one at all. At some point you’ll need to qualify for a credit card and start building up a balance with regular payments to show future creditors and lenders that you are a trustworthy borrower. Not many cards will take chances on immigrants or even young professionals. This is where we at TomoCredit hope to help empower folks towards building a healthier credit history. Our card uses alternative evaluation methods compared to traditional card providers to ensure that you can get a card that will serve you with high rewards and put you on the path to financial success.

College is one of the toughest times to manage your personal finances.

We know this and this is why we interviewed a (relatively) recent college grad and budgeting maestro Sri Ramakrishnan to learn more about his approach regarding college finances and personal tools.

Our conversation here below:

Tomo: Hi Sri, thanks for taking the time to chat with us! How long has it been since you were last in college and what did you study?

Sri: Thanks for having me! I graduated undergrad in 2017 and I majored in Economics.

Tomo: Did you have any jobs or internships during college?

Sri: I did indeed, I had a few jobs through my years in college. I was an English tutor during my sophomore year, worked as a barista at Starbucks for a summer, did a part-time internship at a technology startup alongside my classes during my junior year, and I did a full-time summer internship between my junior and senior year.

Tomo: What were your spending habits like when you were in college?

Sri: To be quite honest, I was (and still am) a fairly frugal individual. Throughout college I’d find ways to stay within specific budgets I had outlined for myself and make sure that I saved a significant percentage of my income when I was working.

That being said, I always made sure to spend money on things that made my life easier or on areas that I felt were investments in myself. Through my senior year, I made a conscience effort to spend more money on experiences that I thought would enrich my life and would become memories I could look back on as opposed to material objects that didn’t give me much joy after the first purchase.

Tomo: Did you have a credit card during college? If so what kind?

Sri: I did but it was just a standard credit card issued by my bank with barely any rewards.

Tomo: Did you use any tools to manage your budget or personal finances during these years?

Sri: During my time in college I didn’t have a specific budget tracker as I do today (I currently manage all my monthly expenses manually on an excel spreadsheet) but I did use a few apps to invest my money and to generally become more financially literate.

I first opened a Robinhood account during my junior year to put my money in a few individual companies I felt very strongly about. I was very compelled by the commission-free trading proposition and wanted to get involved with these stocks that I felt were promising. At the same time I opened an account with Coinbase and invested in Bitcoin and Ethereum after doing a lot of research. This was early in 2017, just at dawn for all the publicity that was brewing around the blockchain/crypto space. For personal transactions and peer-to-peer expenses I used Venmo, as it became impossible to navigate the college landscape without it. Other than these three, I just used my bank’s standard web portal to oversee my expenses and income.

Tomo: Looking back, was there anything you wish you had done differently in regards to your personal finances?

Sri: Honestly, I remember after my senior year vividly wishing I had a high rewards credit card through my time in college. There were so many random expenses from a variety of categories (especially food/travel) that I could have reaped rewards from. On top of this, I was paying the rent for my senior year apartment through Venmo to one of my roommates who would write to our landlord the check for all of us. I figured if I had a high rewards credit card throughout this time, I could have built my credit history through these consistent payments and potentially had secured some cash back.

Tomo: Any tools you wish you had used or had during this time?

Sri: Not to sound cheesy but a Tomocredit card would have been huge for me along with many of my peers during this time in college. I know it was hard for a lot of college students to qualify for high rewards credit cards during our pre-employment years without significant credit history or a credit score. Not to mention for me, especially during my years in college to have had a credit card where I could earn rewards in crypto would have paid off tremendously with the huge bull run for cryptocurrencies experienced in late 2017.

Tomo: Any advice you’d give college students who are trying to manage their personal finances?

Sri: Live within your means and try to save a little bit from every paycheck. Start investing in low cost Index funds as early as you can. Pay off any debt you may have as soon as possible (student loans, credit card etc). Once you have enough of a savings cushion, try to live within your means but don’t forget to go spend money on experiences and with people who will bring you joy. You only have one life so go live it up!

To learn more about budgeting, and personal finance tips you can connect with Sri Ramakrishnan on Twitter and Instagram (@sreezy3000) or reach out to him on LinkedIn.