This school year is unlike any other. For both continuing students and freshmen, the college experience is fundamentally changed and provides new and unique challenges on top of the constant existential dread of just being a student. However, may we find reassurance in the constants of college life, such as the fact that college students are always trying to find new and innovative ways to save a dollar or two. Here are some money saving tips and habits to keep in mind as you navigate the upcoming academic year.

Rent your textbooks

Buying the required textbooks for all your classes every semester adds up quickly. Let’s be honest, does that 600 page Intro to Physics textbook have much practical use when classes are over besides serving as a very expensive paperweight? Know how to get your work done without having to drop cash on textbooks. With most libraries closed at the moment, it’s no longer possible to drop in and do homework using reserve copies.

However, never fear, for there is a solution for you studious folks. Many online retailers offer rental programs, allowing students to borrow textbooks for however long they need. The best part is, you can rent both hardcopy and ebook versions of most textbooks for quite cheap. Hardcopy rentals come with a free return label that you attach to the box it was shipped in when you’re ready to return your books. If you prefer not to worry about shipping your rentals back, ebook rentals are instantly available and can be accessed from any device until your borrowing period ends.

Rent your laptop and wifi

Check if your college has a tech rental or device lending program. Many universities have implemented such programs to ensure students have access to online learning materials. Students in need of essentials such as a laptop or wifi hotspot are encouraged to utilize their college’s resources so that you can continue getting a quality education to the best of your instructor’s abilities.

Bored? Check out your local library

Libraries across the country are online. If you’ve never had a city library card before, it’s better to get one now than never. Learn that language, read that biography you’ve been meaning to read, if we’ve learned anything about ourselves the past 6 months is that it never hurts to take time for yourself. Let the library’s resources help you with that. Also, you’d be surprised at how much your county library has to offer; many of them also offer audiobooks, films, and music!

Student perks

Although it may not seem like it some days, being a student has its perks. Check in with your college to see if they offer free programs such as Adobe Creative Suite or Microsoft Office. These can easily cost you hundreds of dollars out of pocket. Apart from productivity programs, students are also blessed with student discounts from a variety of retailers and companies such as Spotify and Crocs.

Free food!!

Colleges around the country understand how tough it is for everyone right now and are implementing programs to help alleviate some of the issues students are facing as of late. If you are facing food insecurity, check to see if your college has an open pantry or free grocery program. These programs are dedicated to providing students with fresh fruits and vegetables and other pantry staples. Bonus: having all these fresh ingredients will inspire you to strengthen your cooking abilities, which is always a solid skill to have.

Create a monthly budget

At the beginning of each month, evaluate your spending habits. Did you overspend on anything? Have you gone out to eat more often than you intended? You may need to confront yourself. It may be uncomfortable at first, but you will eventually develop a sense of discipline and restraint that will benefit you in the long run. Use the 50/30/20 rule to allocate your budget for the month into the categories of needs, wants, and savings. With this method, you will put 50% of your budget to needs such as groceries and bills, 30% will go to wants like dining out or anything else that is not essential but enjoyable, and 20% is stored away in a savings account. Just remember that this is a general guideline, and everyone has different financial situations.

It’s cheaper to eat healthy

Stocking up on snacks, energy drinks, and instant ramen at the grocery store seems like the cheaper and easier option for daily sustenance. However, there’s a reason the mantra “health is wealth” is so universally lived by. Being mindful of how you are eating has its long term health benefits, sure, but we’re talking about cash here. Fresh produce at a few dollars a pound can go way longer than a frozen meal at the same price. Download the apps of your nearest grocery store and watch how far your dollar can go.

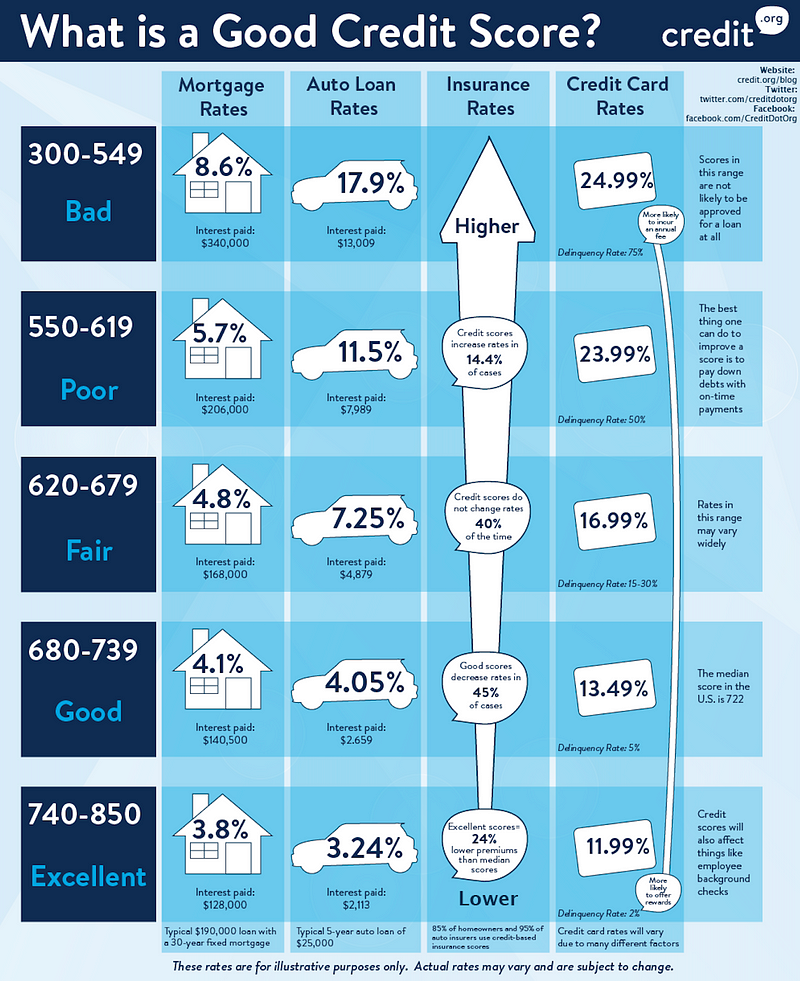

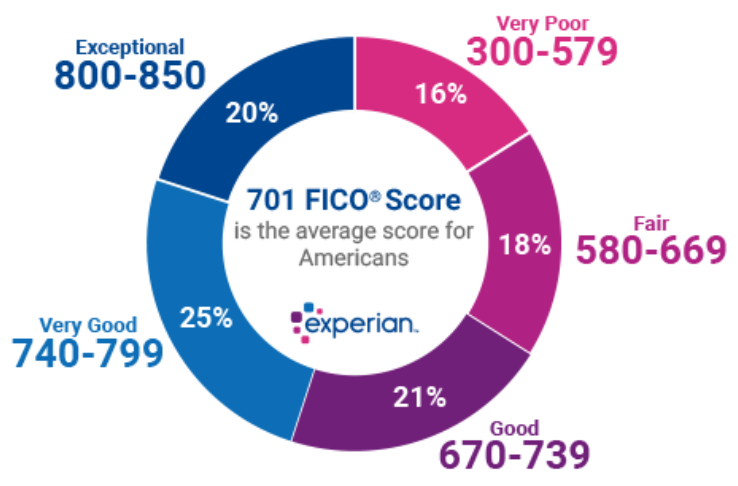

Got credit? Maintain a high credit score!

Perhaps having a high credit score is the last thing on your mind, with exams always around the corner and figuring out what you’re going to eat for dinner. These are present and valid concerns, but it never hurts to prepare for the future. We all know that credit is a delicate game, but if you budget correctly and consistently make on-time payments then the benefits of having a high credit score will follow you even after you graduate! A good credit score means you’ll be paying lower interest on loans and you’ll have a higher chance of getting approved for better rates, saving you a ton of money and stress in the long run. Don’t know where to start? Get pre-approved for Tomo Credit — no fees, no interest, and no credit score needed! Learn more here.