Entering adulthood is an exciting time filled with new opportunities and responsibilities. A significant part of these responsibilities involves personal finance. Recently, an article featured on Supermoney titled “Can I Get A Credit Card At 17?” highlighted how today’s young adults are proactive and thoughtful about planning their financial future. For many young adults, this includes figuring out how to build financial stability while possibly managing the needs of aging parents. It might feel overwhelming, but with the right approach, you can set yourself up for success. Here’s a guide to understanding credit scores, building financial wealth, and balancing the care of senior parents.

Understanding the Credit Score System

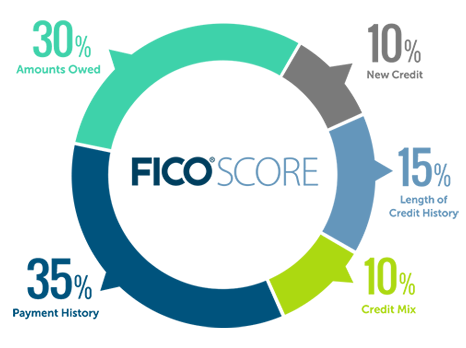

Your credit score is a three-digit number that reflects your creditworthiness—the likelihood that you will repay debts on time. This score plays a crucial role in your financial life, affecting your ability to rent an apartment, buy a car, or even get a job. Here’s how you can start building and understanding your credit score:

1. Get a Credit Card or Become an Authorized User: At 18, you’re eligible to apply for a credit card. If you have a limited credit history, consider starting with a secured credit card, where you deposit money as collateral. Alternatively, ask a trusted family member to add you as an authorized user on their account to benefit from their good credit habits. Kristy Kim, CEO and Founder of TomoCredit also elaborated more that “If you’re a student, there are special credit cards just for you. They’re designed for people starting out, so they often have lower limits and might charge higher interest, but they’re a good way to learn. And even if you’re not ready for a credit card, managing a savings or checking account responsibly shows banks you’ve got your money game on point. It’s all about showing you’re responsible with money. Learn about credit, maybe take a course, or read up online. And don’t hesitate to ask your parents or guardians for advice—they’ve been there and can help you navigate this whole credit thing until you’re ready to fly solo.”

2. Pay Bills on Time: Payment history is the most significant factor in your credit score. Always pay at least the minimum payment on your credit card by the due date. This habit will help you build a positive credit history.

3. Keep Credit Utilization Low: Your credit utilization ratio—how much of your available credit you’re using—also impacts your score. Aim to use less than 30% of your credit limit to maintain a healthy score.

4. Monitor Your Credit: Regularly check your credit reports for accuracy and to understand how your actions affect your score. You can get a free credit report once a year from each of the three major credit bureaus at AnnualCreditReport.com.

Building Financial Wealth as a Young Adult

As you embark on your financial journey, it’s crucial to adopt a long-term perspective and focus on building wealth gradually. Achieving financial stability and growth doesn’t happen overnight; it requires consistent effort, discipline, and smart decision-making. Whether you’re just starting with your first paycheck or thinking about your future financial goals, every step you take now lays the foundation for lasting financial security. Here are some essential steps to help you get started on the right path:

1. Create a Budget: Track your income and expenses to understand where your money is going. This habit is foundational for managing your finances effectively and identifying areas where you can save.

2. Start Saving Early: Even if you can only save a small amount, start putting money aside in a savings account or an emergency fund. Over time, this will provide you with a financial cushion for unexpected expenses.

3. Invest in Your Future: Consider opening a retirement account, such as a Roth IRA. While retirement may seem far off, the power of compound interest means that starting to invest at 18 can significantly grow your wealth over time.

4. Educate Yourself: Financial literacy is crucial. Take the time to learn about investing, taxes, and personal finance. There are many free resources online, including blogs, podcasts, and courses, that can help you build your knowledge.

Balancing Financial Responsibilities with Caring for Senior Parents

If you have senior parents who may need your support, it’s important to balance their needs with your financial goals. Here’s how to approach this situation:

Managing the responsibilities of caring for senior parents while pursuing your own financial goals requires a combination of open communication, strategic planning, and seeking appropriate support. Start by having candid conversations with your parents about their financial situation and healthcare needs. Gaining a clear understanding of these factors will allow you to plan and budget more effectively. Additionally, researching government programs and non-profit organizations that provide financial assistance, healthcare, or caregiving support for seniors can be highly beneficial, as these resources can help ease some of the financial strain you may encounter. As highlighted in a recent GoBankingRates article, “7 Ways Millennials Can Budget Time and Money When Caring for Boomer Parents” TomoCredit emphasizes that local community resources can also offer valuable support.

Once you have a clear understanding of your parents’ needs, create a caregiving plan that includes budgeting for their healthcare, transportation, and daily living expenses. It’s wise to involve other family members or friends in this process to share responsibilities and ensure a comprehensive plan. While it’s important to prioritize your parents’ care, it’s equally crucial not to lose sight of your own financial goals. Striking a balance between supporting your parents and building your own financial future is key to long-term stability.

If managing these responsibilities becomes overwhelming, consider seeking professional help. Financial advisors or eldercare planners can provide valuable advice on how to manage your finances while supporting your parents. They can also assist in navigating complex situations, such as Medicaid planning or securing long-term care insurance, ensuring that both you and your parents are well-prepared for the future.

At early adulthood, you have a unique opportunity to build a strong financial foundation that will serve you throughout your life. By understanding the credit score system, taking steps to build wealth, and thoughtfully balancing the needs of your senior parents, you can set yourself up for financial success. Remember, it’s a journey, and every small step you take now will have a significant impact on your future.

Stay proactive, seek advice when needed, and always keep your financial well-being in mind as you navigate the challenges and opportunities of adulthood.